YouGov: Annual health check for the industry

YouGov’s Charlie Dundas reflects on the performance of the betting sector in 2019

Given that this is our last column for 2019, we thought it would be interesting to review some of the 16 metrics we track against betting brands every day by looking at the performance of the sector as a whole over the past 12 months.

It’s worth noting here that the figures we’ve produced for the sector’s overall performance may mask the performance of individual brands. If you want a brand’s individual data, please get in touch.

As we’ve written before, the betting sector is not without its challenges in public perception. Most people have a poor view of the industry and this is reflected in its negative score for our Impression metric (which asks if people have a positive or negative view of a brand and calculates a net score).

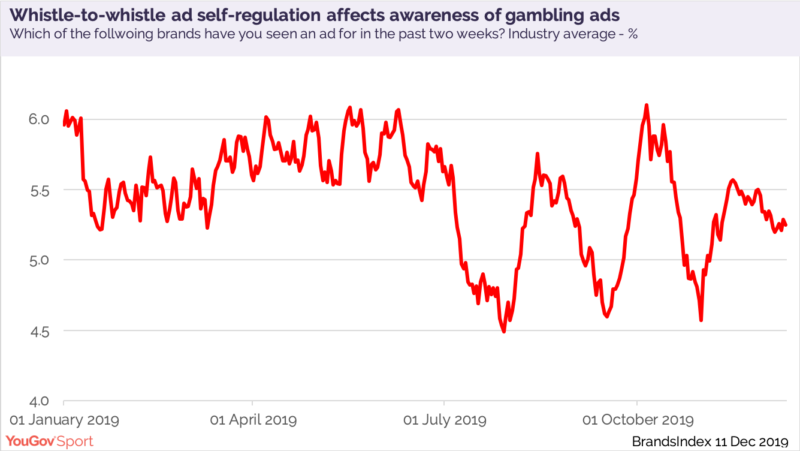

If you’re looking for a silver lining, it’s that the sector’s score increased over the course of 2019, edging up almost a couple of points – so the overall trend is one of improvement. Another metric worth looking at in a year in which new voluntary measures on advertising came into place is our Ad Awareness metric, which asks respondents if they have seen an advert for gambling brands in the past two weeks.

The score for this metric has indeed become more volatile since August this year. And although the peaks of Ad Awareness have reached the same levels seen before the changes – for example,

when Wayne Rooney joined Derby, with branding from 32Red – there are dramatically more troughs for this metric than there were before the change.

On the other hand, our Awareness (rather than Ad Awareness) metric tells a slightly different story. It records that awareness of brands across the sector (so taken as a whole) has remained almost exactly steady, running at about 55% throughout 2019.

No harm done

So, with these different data points suggesting different outcomes, has self regulation affected market size? Not according to information from further down the purchase funnel. As we would expect, our Current Customer metric, which asks if people have used a brand in the past six months, has shown some volatility using a four-week average. For example, it peaks following the Grand National; again in July this year (perhaps reflecting the busyness of the sporting calendar in 2019); and once more at around the time of the Rugby World Cup.

But when using 26- and 52-week average scores, which take in a greater range of data into the calculation of a trend, the line for the sector’s Current Customer score is almost entirely flat. And while that’s not the growth the industry would wish for, it does imply that it has not been harmed by self-regulating around whistle-to-whistle advertising.

Finally, let’s look at our overall indicator of brand health for the sector, its Index score. Index is a composite of all six brand health metrics and, as a result, it gives us a good feel for how a brand or group of brands is performing overall. Using a four-week average, again we see a small degree of volatility over the course of this year, with a range of three points between peaks and troughs. But

using a 26-week view of the data, apart from a one-point dip at the beginning of 2019, it’s been pretty plain sailing for the industry as a whole.

In summary, then, 2019 was a year of reputational stasis for the industry and that’s no bad thing for a sector which faces so much scrutiny. But with ground to make up on other sectors, industry leaders will be looking to build on these scores for 2020. As ever, we’ll be keeping a close eye on the data.

Charlie Dundas is commercial director at YouGov Sport, the sports and entertainment division of global research and insight agency, YouGov. YouGov Sport tracks the public’s perceptions of sports events, leagues, teams and athletes every day in markets across the world on a daily basis.